The Market Has Underestimated the Strength of the US Economy

Published: Wed, 09/07/22

The Market Has Underestimated the Strength of the US Economy

US President Joe Biden speaks at a meeting with business leaders on Thursday, July 28, just as the drumbeat of recession grew louder. Photographer: Oliver Contreras/Bloomberg

By; Edward Harrison

US economic data show that consumers continue to spend and that this spending is backed up by a robust job and wage picture. Forget about being in a recession. If it weren’t for inflation, this would be a Goldilocks environment.

The US economy is resilient

Shares are now well below their August highs even as Wall Street appears to have underestimated the resiliency of the US economy. With leading economic indicators pointing firmly lower, the real test for markets still lies ahead. For equities, Goldilocks might be a mild recession followed by a period of slow growth. Anything better will invite an over-tightening that hurts the economy and asset prices.

Alas, we have a pretty big inflation problem. And that means higher interest rates and the likelihood that any resilience won’t last. From a market perspective, I see two outcomes. In the fixed-income market, US economic data must continue to show strength for the Treasury curve to continue to steepen. That would mean higher discount rates for future cash flows, which impacts the equity market. All shares would be under pressure and high-beta stocks would lag, especially as an evaporating “buy the dip” mentality bites. But when the steepening wanes and the economy turns down, the yield curve will flatten. Eventually Goldilocks could return, but only in the form of a growth recession.

Wall Street gets caught being too bearish on the economy

You could make the argument that the collective wisdom of a forward-looking market sniffed out the recent growth uptick. Stocks bottomed in mid June, whereas the first inkling we got that the third quarter was off to a good start wasn’t until the Atlanta Fed’s GDPNow tracker on July 29 that started at 2.1% growth.

This was literally the day after we saw a second consecutive decline in US quarterly GDP. Lots of people were telling us the US was already in a recession. But the rally in shares was telling another story.

In the weeks since then, the GDPNow numbers have improved to where, based on available data, the Atlanta Fed’s model would predict a 2.6% annualized rise in GDP for this quarter. If anything, Wall Street was too bearish.

Why are stocks going down now?

Yet, stocks peaked in mid-August and are now headed down. I don’t think that’s just a reflection of higher interest rates. It’s a warning that stocks should fear a Fed that has the labor market on its side. An improving economy means more rate hikes as long as inflation remains elevated. Shares will get hurt either through higher discount rates or from the lower earnings engendered by inflation and rates cooling growth. In essence, it will be hard to maintain a Goldilocks outcome unless the Fed relents. That’s a big part of why the market is jittery.

You can see this in operating margins. Bloomberg Intelligence recently published a report showing that “rolling four-quarter operating margins for the S&P 500 (excluding energy stocks) have decreased steadily under the weight of inflation this year”. Analysts are hoping, even expecting, an upturn starting next quarter — perhaps due to improving data prints. But that lift will depend on interest rates as well as on inflation and the ability to mitigate its effects.

As that uncertainty plays out against the backdrop of rising rates, we should expect the S&P 500 to re-test 2022 lows. But it’s the resiliency of the economy and the path of inflation and interest rates which will determine whether shares break down meaningfully and exceed the lows or regain strength.

Buy the dip is taking a beating

In the meantime, we’re seeing a mental shift in the equity markets now. As the high-beta stuff like Peloton, Robinhood, Lyft, and Beyond Meat collapsed to lows 70, 80 or 90% below all-time highs, many retail investors kept the faith. Yes, we saw some outflows from exchange-traded funds like the Cathie Wood’s ARK Innovation ETF (ARKK) last year, but we were still seeing inflows in most of 2022.

However, last month ARKK saw its biggest monthly outflow since last September.

That’s a sign that investors have given up waiting for a return to the surges in high-beta shares, meme stocks or crypto assets which characterized pandemic trading. Instead of buying the dip, they are re-allocating funds to less volatile shares and asset classes.

With retail investors less in the driver’s seat, shares are more exposed if earnings or rates bite. Given the diminishing number of investors looking to buy speculative bets on the cheap after repeated losses from that strategy, shares should fall if the discount rate of future cash flows continues to increase.

So, is this all about interest rates now?

It’s tempting to pin all of recent equity market weakness on discount rates. After all, the Bloomberg bond index last week dropped 20% from its January 2021 peak. Global bonds are having their first bear market in a generation. But the selloff in equities started well before the Fed’s hawkish Jackson Hole remarks.

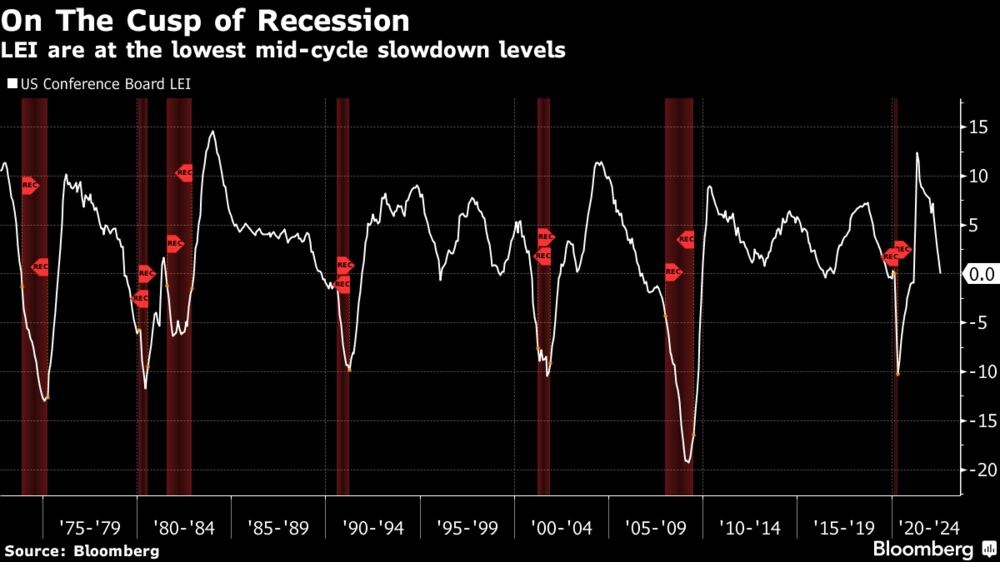

I look at the recent weakness as more of a resumption of a fundamental trend after a bear-market rally which transpired because of a brief resurgence in the economy. If you look at the Conference Board’s Leading Economic Indicators, for example, the downtrend is unabated.

The base case still has to be a situation in which the US economy falls into recession. In terms of the leading economic indicators, we’re right at the level separating mid-cycle slowdowns from recessions. And with the slope of the line aggressively negative, it would take a remarkable turnaround to stop here. So the decline in shares is not all about rates. It’s due to a fundamental downtrend in growth that has been lessened this quarter, but only temporarily.

The hard part is knowing what comes next?

Because leading economic indicators are still falling precipitously amid a growth uptick, it’s hard to know what comes next. This is one of those perverse ‘good news is bad news for stocks’ environment. The more robust the data, both on the employment and inflation front, the more likely we are to reach new 10-year Treasury yield highs. And that is trouble for the economy and stocks, especially the most volatile shares.

In the past few weeks, as the market started to figure out that the third quarter would be pretty good, long-term Treasuries sold off the most and the curve steepened nearly 30 basis points.

Still, the curve remains inverted. That’s the market reacting to positive data flow, but still telling us expectations are for a recession. That has seen 10-year Treasury yields rise nearly seven-tenths of a percentage point. We’re now less than three-tenths of a percentage point away from cycle highs on the 10-year yield.

For me, the best way to reconcile an inverted yield curve’s recession signal with this rise in rates is by looking at this in terms of inflation and the policy response. As I wrote on the Bloomberg Terminal in July:

whether we have hit peak rates ultimately depends on how well markets have gauged the Fed’s eventual policy path and the terminal rate. Persistent inflation and a more aggressive Fed will mean 10-year yields can go higher than 3.50%, leading to a deeper recession and another selloff in equities.

A new high in yields strongly hints at a deeper or more protracted downturn, which would make new equity lows seem likely. The speculative stuff would fall more than everything else.

But the outcome I expect is one in which this steepening comes to an end relatively soon as economic data soften again. The ‘Goldilocks version’ of my base case sees a so-called “growth recession”, which may be the Fed’s new target. Think of this as a ‘softish landing’ via a mild recession followed by a period of tepid growth — which, (one would hope) many companies can weather because inflation would slow.

In this Goldilocks outcome, stocks don’t get crushed, nor do bonds. Savers do pretty well though. That may not be the Goldilocks some investors want to see after torrid pandemic gains, but it’s still pretty decent.

Quote of the Week

“There certainly seems to be a slight shift in where the Fed thinks the current ‘restrictive’ threshold would be. Powell’s Jackson Hole speech said clearly that 2.5% would be far short of where ‘restrictive’ would be given high inflation today.”Anna Wong

Bloomberg chief US economist